Spending vs. Investing in Your 20s: What’s the Smart Choice?

How much of your spending on electronics is actually worth it? And how can early investment help you gain more control over your financial decisions?

In this blog, we’ll explore the advantages of starting your investment journey early—and the opportunity cost of spending heavily on lifestyle upgrades instead.

Most of us in our 20s feel the urge to splurge on the latest gadgets to look cool in our social circle. But in doing so, we adopt a spending-first mindset, investing in devices that often lose relevance or value every 2–3 years due to rapid tech upgrades.

How Early Investment Helps You Achieve Big Financial Goals

📘 Early Investment Scenario #1: X vs. Y

Let’s understand this with a simple example featuring two individuals: X and Y. Both get placed in private companies with a monthly salary of ₹30,000 each. However, their lifestyle choices and money habits are completely different.

X believes in building financial stability. He educates himself through passive income ideas and starts investing 20% of his salary into mutual funds early and direct equities. His goal is long-term wealth and financial freedom.

Y, on the other hand, prioritizes lifestyle. He spends heavily on expensive smartphones, branded clothes, and non-essential items—amounting to 60% of his monthly income.

Now imagine both individuals stick to these habits consistently for the next five years.

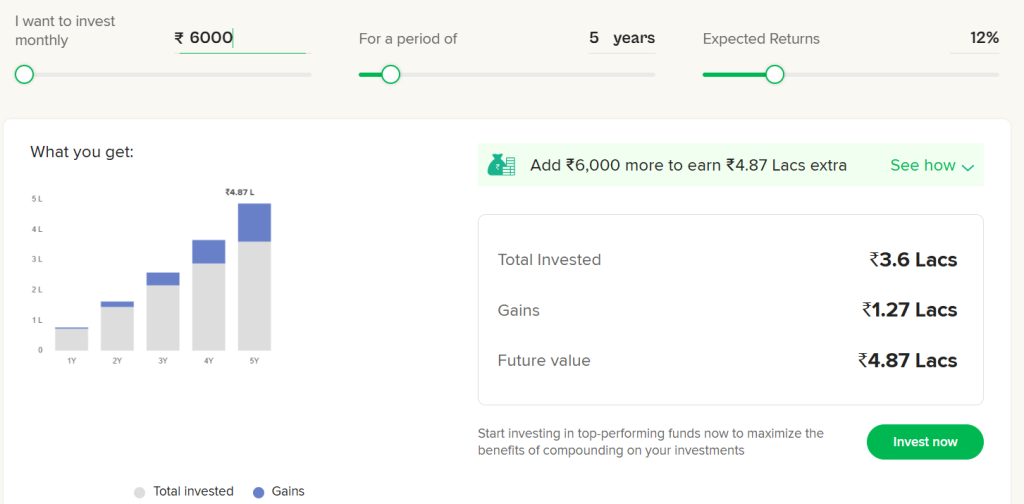

Assuming equity investments yield an average return of 12% per annum, and considering the power of compounding, Mr. X will accumulate a substantial corpus—running into lakhs—while Mr. Y will struggle with savings.

Mutual Funds calculator with expected returns in five years.

Mr. Y needs to invest double the amount in less time to get most amount for the same duration.

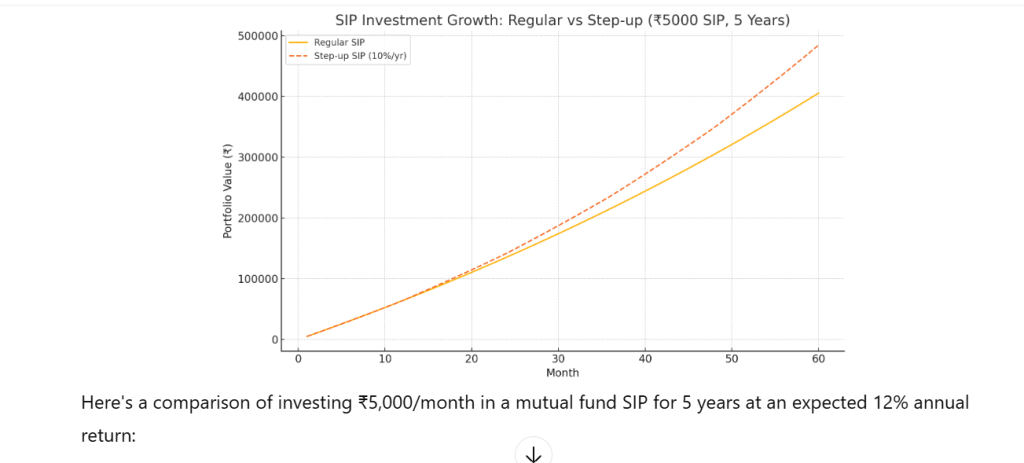

📊 Scenario #2: Traditional SIP vs Step-up Investment Strategy

Let’s consider a second investment scenario involving Mr. X and Mr. Y, both committed to long-term investing—but with different approaches.

Mr. X follows a traditional SIP (Systematic Investment Plan), investing the same fixed amount every month over several years. His strategy is consistent, simple, and easy to manage.

Mr. Y, however, opts for a step-up SIP strategy. He increases his monthly investment by 10% every year, aligning it with his growing income. This allows him to leverage the power of compounding on a higher base over time.

🔍 What Happens Over Time?

While Mr. X sees steady portfolio growth, Mr. Y’s incremental contributions accelerate his returns significantly—especially in the later years. With the same investment duration and expected return (say 12% annually), Mr. Y ends up with a much larger corpus simply by increasing his SIP gradually.

🧠 Key Insight:

A step-up investment plan is ideal for those expecting annual income growth, as it helps build wealth faster without feeling financially burdened in the early years.

📊 Investment Scenarios Compared

Scenario

Final Value (5 Years)

Total Invested

Growth Achieved

Regular SIP

₹4,05,518

₹3,00,000

₹1,05,518

Step-up SIP (10%)

₹4,84,590

₹3,65,500

₹1,19,090

Investment and returns comparison for regular and step-up SIP

Image the duration is increased to longer duration returns from Step-up SIP will increase drastically compared to Regular SIP

⏳ Investment Scenario #3: Doubling the Duration for Bigger Gains

When it comes to wealth building, extending your investment horizon is one of the most powerful strategies. The longer your money stays invested, the harder it works for you—thanks to the magic of compound interest.

Let’s revisit our familiar example featuring Mr. X and Mr. Y, both following the same investment strategies as before:

Mr. X: Regular SIP with a fixed monthly contribution

Mr. Y: Step-up SIP with a 10% annual increase

🔄 Doubling the Duration: 5 Years vs. 10 Years

What happens if both investors extend their investment duration from 5 years to 10 years, without changing their strategy?

By the time they turn 30 years old, their portfolios grow exponentially.

📊 Final Portfolio Values

Plan Type

5-Year Value

10-Year Value

Total Invested

Regular SIP

₹4,05,518

₹11,20,179

₹3,00,000 (5Y) ₹6,00,000 (10Y)

Step-up SIP (10%)

₹4,84,590

₹16,34,449

₹3,65,500 (5Y) ₹8,40,000 (10Y)

🔍 That’s nearly 3x growth in Mr. X’s portfolio and more than 3x in Mr. Y’s, simply by staying invested for a longer duration.

🧠 Key Insight:

Time in the market beats timing the market. Even modest SIPs, when held for 10+ years, can build significant wealth.

🕒 Investment Scenario #4: The Cost of Starting Late

One of the most overlooked aspects of wealth creation is when you start investing. While returns depend on the investment and market performance, time plays the most powerful role.

Let’s understand this with a simple scenario:

Imagine two individuals — Early Investor (A) and Late Investor (B) — both aiming to build the same wealth corpus by age 40.

Investor A starts early, say at age 25, and invests a modest amount consistently for 15 years.

Investor B delays investing and starts at age 30. To match Investor A’s target amount, they’ll have to invest almost 2.5x more every month for a shorter period (10 years).

📉 Why This Happens:

Because compounding rewards time, not just the amount. When you delay, you lose out on years of interest-on-interest growth—and have to compensate by investing much more aggressively.

📌 The same returns require higher monthly contributions and more financial pressure for late starters.

📸 Visual Insight:

Below is an image that clearly illustrates how delaying your investment increases the required investment amount to reach the same financial goal:

Two years returns to achive the same returns of an early investment.

🧠 Key Insight:

The earlier you start, the less you need to invest. Time in the market is the biggest multiplier for your money.

🎯 Key Takeaways from All Scenarios

From all the examples above, it’s clear that starting early gives you more control, flexibility, and higher returns over time. Let’s recap the key lessons:

💬 Your Turn

Which scenario resonated most with you? Are you a Mr. X or a Mr. Y today—and who do you want to become in 5 years?

I'm a content creator, blogger, and financial enthusiast who writes about personal finance, investing, stock market trends, and self-improvement on my blog Wealthy Wisdom. With a strong interest in simplifying financial concepts for everyday readers, I focus on topics like SIP strategies, asset allocation, mutual fund selection, and regulatory updates (SEBI, UPI, F&O, IPOs, etc.).